What Is a Perpetual DEX?

Key Takeaways

A perpetual DEX is a decentralized exchange where traders can access perpetual futures directly from a self-custodial cryptocurrency wallet, rather than depositing assets with a centralized exchange.

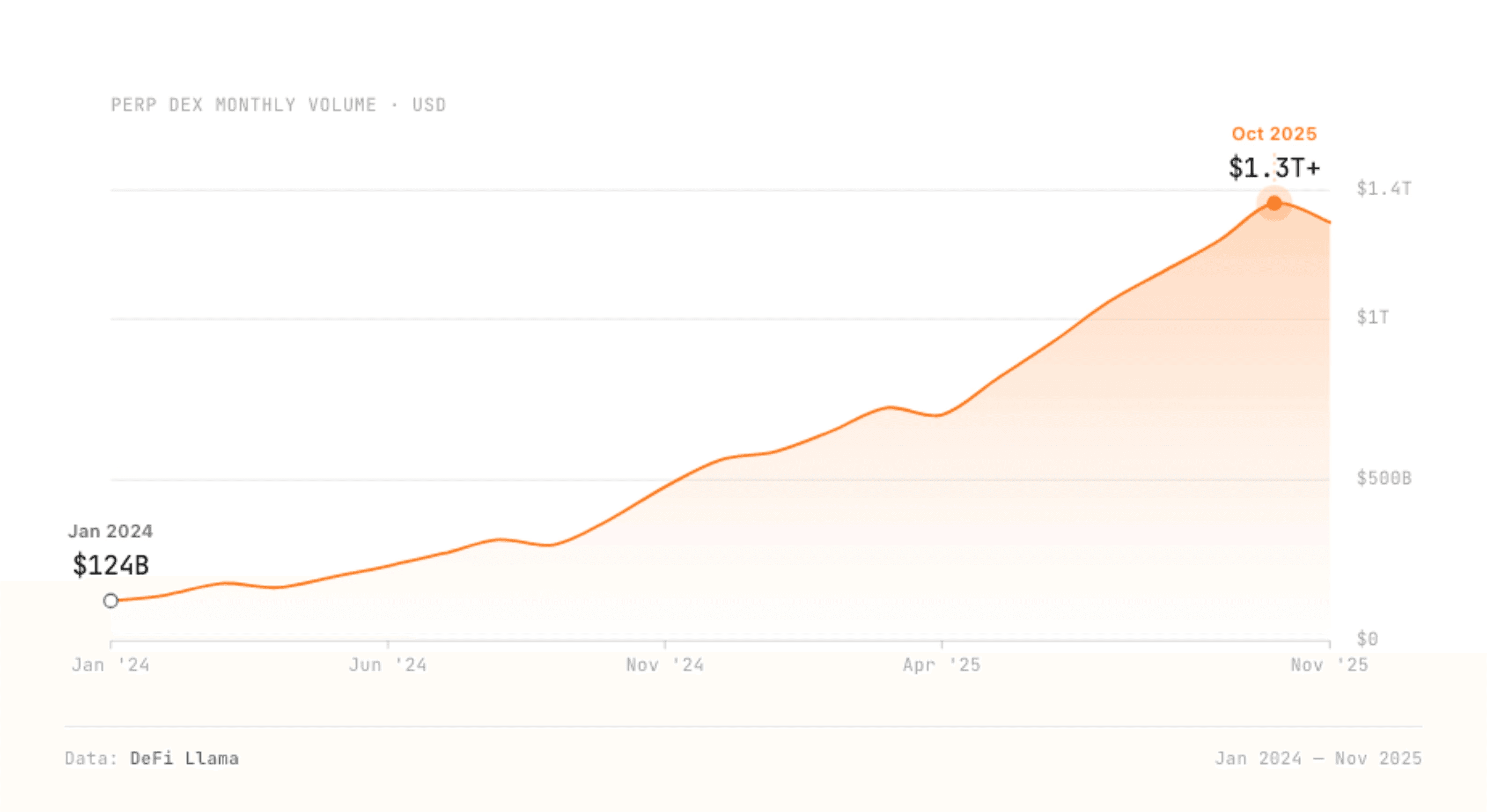

The perpetual DEX sector has grown rapidly: monthly trading volume rose from $124 billion in January 2024 to more than $1.3 trillion in November of 2025.

Most perpetual DEXs rely on four core functions: a trading engine that prices, matches, or executes trades; a margin system that tracks collateral; an oracle that supplies market prices; and a liquidation engine that closes under-margined positions.

Perpetual DEXs use one of two main architectures: an on-chain or hybrid central limit order book (CLOB), the same model as Nasdaq and the NYSE, or an automated market maker (AMM) using virtual liquidity pools. Each has different liquidity, capital efficiency, and execution trade-offs.

Since mid-2025, the market has shifted toward CLOB architectures. As of April 2026, the majority of top perpetual DEXs by total volume run on order books (DeFi Llama).

What is a perpetual DEX?

Most perpetual futures volume still flows through centralized exchanges, but that's changing fast. Decentralized perpetual exchanges grew from roughly 2% of the market in 2024 to over 10% by early 2026, with monthly volume crossing $1 trillion for the first time in October 2025.

A perpetual DEX (sometimes called a "perp DEX") is a decentralized trading venue where traders can access perpetual futures contracts (leveraged derivatives with no expiration date) without going through a centralized intermediary like Binance, Coinbase, or Bybit.

At a centralized exchange (CEX), a trader deposits funds into the platform's custody and trusts the exchange to keep those funds safe and to execute and settle trades. A perpetual DEX works differently. Traders connect their own cryptocurrency wallet, and trades execute directly through smart contracts or on-chain matching engines. In many perpetual DEX designs, traders interact through a self-custodial wallet and do not open a traditional exchange account, though frontends may restrict certain jurisdictions or features.

The "perpetual" in perpetual DEX refers to the type of contract being traded. A perpetual futures contract, or "perp," tracks the price of an underlying asset like Bitcoin, gold, or a stock, and can be held indefinitely – unlike traditional futures contracts, which expire on a fixed date. To keep the contract price aligned with the underlying market, perpetual futures use a mechanism called the funding rate.

"DEX" is shorthand for decentralized exchange. On a decentralized exchange, functions such as settlement, collateral accounting, and liquidations are handled by smart contracts or publicly auditable protocol infrastructure rather than only by a private exchange database. Depending on the architecture, trades, liquidations, funding payments, and settlement events are either recorded on-chain or made publicly auditable through protocol infrastructure. That gives users more transparency than a centralized exchange's internal ledger.

The first decentralized perpetual futures market launched on April 20, 2020, when dYdX’s BTC-USDC perpetual market entered its private alpha, almost exactly four years after BitMEX pioneered the perpetual future on the centralized side. The launch became accessible to the public shortly after in May and offered up to 10x leverage on Bitcoin with USDC collateral. dYdX billed it as "the first ever decentralized Perpetual Contract Market."

A wave of competitors followed in the years after, each experimenting with a different architecture, and the category has since grown from a niche DeFi experiment to one of the fastest-growing segments in crypto.

How Perpetual DEXs Work

Most perpetual DEXs have four essential components working together: a trading engine, a margin system, an oracle, and a liquidation engine. Each handles a distinct piece of the trade lifecycle.

The Trading Engine

The trading engine is where orders get priced, matched, or executed. How that happens depends on the chosen architecture. CLOB-based DEXs run an order book: traders post bids and asks, and the engine matches compatible orders. AMM-based DEXs work differently. Rather than matching counterparties, they price trades against a shared liquidity pool using protocol rules and oracle inputs.

The Margin System

The margin system tracks a position's collateral and profit or loss in real time. When a trader opens a leveraged position, they post collateral (margin) that backs the trade. As the underlying price moves, the margin system updates each position's status continuously. If equity in the position falls below the venue's maintenance margin requirement, the system flags it for liquidation.

The Oracle

A perpetual DEX needs accurate, up-to-date price data for every underlying asset it lists. That price feed comes from an oracle: a system that brings external data, like the market price of an asset, on-chain. Modern perpetual DEXs source pricing from networks like Chainlink and Pyth Network, which aggregate quotes from major exchanges and market makers and stream price updates on tight intervals, often sub-second. The quality of the oracle directly affects the fairness of liquidations and the accuracy of funding rate calculations.

The Liquidation Engine

When a trader's equity falls below the minimum required to support the position, the liquidation engine is designed to close part or all of the position before losses exceed posted collateral. This protects the exchange from accumulating bad debt and keeps the system solvent. Some perpetual DEXs use partial liquidations, where the engine closes only enough of the position to restore margin requirements rather than closing the full position at once. This reduces the amount of capital lost to liquidation events and keeps traders in their positions longer.

In many DEX designs, liquidations are triggered by protocol rules, and the resulting transaction or state change is publicly auditable. That reduces reliance on an exchange's private internal ledger, though the exact liquidation process varies by venue.

DEX Architectures: Order Book vs AMM

Perpetual DEXs can be designed in several different ways. The biggest architectural divide is between order book DEXs and AMM-based DEXs. The choice has meaningful implications for liquidity, capital efficiency, and execution quality.

Order book DEX (CLOB)

A central limit order book, or CLOB, is how traditional exchanges like the New York Stock Exchange and Nasdaq have long worked. Buyers and sellers post limit orders at specific prices, and the exchange matches them to a counterparty when those prices are hit. Participants can see how many orders exist at every price level through an order book.

CLOB-based perpetual DEXs adapt this same model, either fully on-chain or in a hybrid architecture.

Pros

Deep liquidity, provided market makers are active

Tight spreads

Predictable execution

Familiar to traders migrating from a CEX

Cons

Difficult to run fully on-chain at high frequency due to blockchain throughput and gas costs

Many CLOB DEXs run their matching engines off-chain or on purpose-built chains, which introduces different trust, latency, and transparency trade-offs

Examples of CLOB perpetual DEXs: Aster, dYdX, Hyperliquid, Lighter, and GTE (testnet).

AMM-based DEX

An automated market maker (AMM) replaces the order book with a mathematical pricing formula and a liquidity pool. For perpetual futures, AMMs use virtual liquidity pools or other hybrid designs to simulate price discovery without requiring a full order book.

Pros

Can be implemented mostly or fully on-chain, depending on the design

Simple to implement

Anyone can provide liquidity (no need for dedicated market makers)

AMMs can be easier to bootstrap in new or long-tail markets because liquidity can come from pooled capital rather than a standing network of professional market makers.

Cons

Wider spreads

Higher slippage on large trades

Greater dependence on oracle design and liquidity-pool mechanics, which can affect execution quality during volatile markets.

Examples of AMM-based perpetual DEXs: GMX, Perpetual Protocol, Gains Network

Why does it matter?

For small trades on highly liquid pairs, the architectural difference may not be obvious to the average trader. Either architecture will execute the trade quickly and at a reasonable price.

For larger retail traders, institutional market makers, and professional trading firms, the architecture matters a lot. Order book DEXs support passive limit orders, maker rebates, and enable complex strategies (basis trades, market making, advanced hedging) that AMM-based offerings are less naturally suited to.

Recent volume has favored order-book designs. By Q1 2026, the top three perpetual DEXs by trading volume (Hyperliquid, Aster, and edgeX) were all running CLOB-based architectures, and CLOB venues account for the majority of total perpetual DEX volume (DeFi Llama).

The Trading Flow

From the trader's perspective, placing a trade on a perpetual DEX is functionally very similar to doing the same on a centralized exchange. The five-step flow:

Connect a wallet. Rather than logging in to an account or linking a bank, the trader connects a self-custodied crypto wallet (MetaMask, Phantom, Rabby, or similar) directly to the DEX. On many venues, this avoids the account-opening flow of a centralized exchange, though frontend access rules vary.

Make a deposit. The trader moves a stablecoin like USDC or USDT from their wallet into the DEX's smart contract. The trader keeps self-custodial control over account interactions, while the protocol locks deposited collateral according to its margin rules.

Choose a market and leverage. The trader selects an asset from the available list and sets the desired leverage. For example, BTC/USD with 10x leverage.

Place the trade. The trader chooses between a market order or a limit order and decides whether to go long or short. The DEX's matching engine fills the order and the position opens.

Monitor and close. The position's profit and loss, funding payments, and liquidation price update in real time. The trader closes the position whenever they choose — unless the price reaches the liquidation level first, at which point the liquidation engine force-closes the trade.

Depending on the venue's architecture, settlement events, collateral changes, liquidations, and other state updates may be recorded on-chain or made publicly auditable.

Perpetual DEX vs Perpetual CEX

Most retail traders today still use centralized exchanges like Binance, Bybit, or OKX for perpetual futures. Perpetual DEXs offer a structurally different model. The core differences come down to three areas:

Custody

On a CEX, the platform holds the trader's funds in exchange-controlled wallets. On a DEX, the trader connects a self-custodial wallet and posts collateral to a smart contract or protocol account governed by transparent margin rules.

Access

CEXs are typically restricted by geography and require account creation, KYC verification (government ID, sometimes a selfie or proof of address), and in some cases minimum deposit thresholds. Perpetual DEXs are often permissionless at the protocol level, though access can vary by jurisdiction.

Transparency

On a CEX, trades, funding payments, and liquidations are recorded on the exchange's internal ledger. Many perpetual DEXs record every action on a public blockchain, where any trade, funding payment, or liquidation can be independently verified.

_____________________________________________________________________________________________

The trade-offs run in both directions. CEXs typically offer the deepest liquidity, the lowest latency, and the broadest fiat on-ramps. Perpetual DEXs offer self-custody, permissionless access, and greater transparency and they're closing the execution gap quickly.

A new generation of perpetual DEXs is closing the execution gap with centralized venues. GTE is one example of this newer CLOB-based category. Currently in testnet, it is designed for perpetual futures across crypto, equities, commodities, and prediction markets.